Would you prefer to receive $1,000,000 or a magical penny that doubles in value for 31 days?

This question is the basis for some of my favorite lessons when I’m teaching personal finance workshops to undergrads, grads, and employees. Let’s see if you can guess the answer too!

Wandering on the street one day, you notice a shiny penny on the sidewalk. When you pick it up you learn that this isn’t an ordinary penny, but a magical one. The power of this penny is that it doubles in value each day for a month. In other words, when you wake up the next day, you miraculously have two pennies; on day three, four pennies; on day four eight pennies, and so forth.

I ask attendees to estimate how much the magical penny is worth at the end of 31 days and then poll the audience to see which option people prefer: the magical penny or a one-time payment of $1,000,000.

Which would you take? After you decide, scroll down beyond the image of the penny below to see the answer.

Ready?

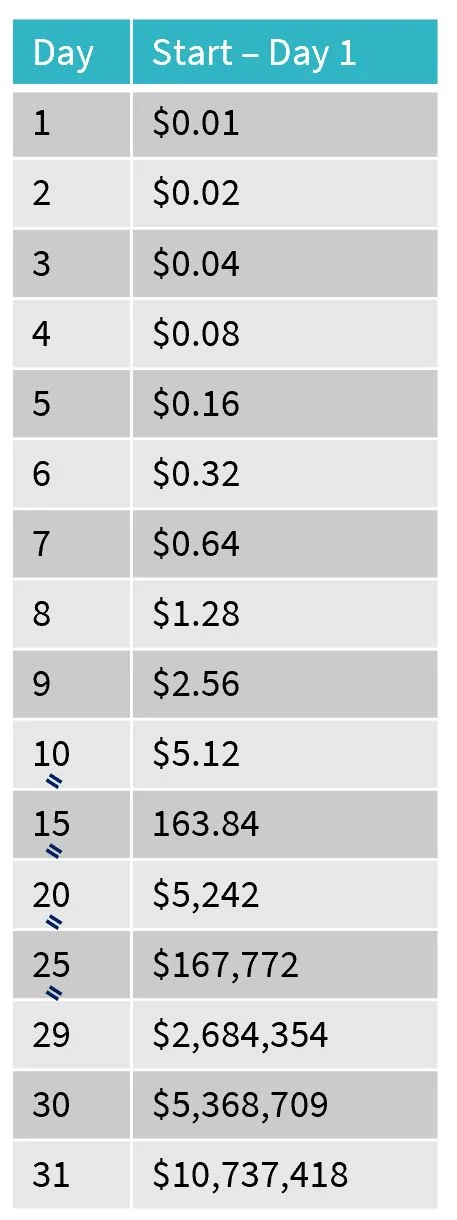

The magic penny would be worth over $10 million dollars! In other words, you would unequivocally be better off taking the magic penny than a one-time payment of $1,000,000!

If you don’t believe me, you can calculate the answer with brute force, look at the summarized table below, or follow the link to this online spreadsheet if you want to see the full calculation).

I use the penny example primarily to illustrate the power of compounding and how important the time value of money is when it comes to investing for retirement; however, the beauty of the magical penny is that it offers many other lessons too.

Primary Lesson: Investing Early Is Crucial

Saving early is perhaps the most important retirement axiom in personal finance. The magical penny not only provides a vivid example of the sheer power of exponential growth, but also helps reinforce the value of early savings.

Imagine what would happen if you missed the magical penny on the first day and only picked it up on the second day (and, therefore, only had 30 days for it to double). You would only end up with half as much money or a little over $5 million. The easy way to intuit this is to think that you are essentially missing out on the last day of doubling (the online spreadsheet I created shows the full calculation for this scenario too).

Or, imagine what would happen if you missed the magical penny and only picked it up on the tenth day. The answer: you would only have ~$20,000!

As you can see from the chart above, the last few days of the month are where your total balance really starts to grow fast. The important insight is that while the last doubling provides the largest growth in dollars, you only get to it if you had started to save early.

Lesson 2: Delaying Has Consequences

The corollary to the need to save early is that a delay of a few years can have drastic consequences and may require you to divert additional funds to catch-up.

Look at Day 10 of the magic penny chart. To catch up to someone who found the penny on Day 1 you would need to start with $5.12 instead of $0.01. While that may not seem like a large difference because of the scale, it is orders of magnitude more.

(At this point, I usually switch the participants to more relatable numbers and growth rates, like an example where they invest $2,000 a year and it grows at 6% on average)

Lesson 3: Small Amounts Add Up

Often, the students or employees to whom I’m speaking may not be in a position to put large amounts into a retirement account right away, let alone max out a 401(k) every year. Many are struggling to navigate competing demands for their money including paying off student loans, saving for retirement, and helping their families. Some get intimidated and mistakenly think that if they can’t put away the maximum amount, they might as well not save anything.

I use the penny example to reduce their anxiety and discuss how their savings choice is not binary. What the magical penny confirms is that small amounts add up quickly over time. Yes, a lot may be better than a little, but something is also better than nothing. Furthermore, you can always increase your savings rate over time. In other words, amount in market is important, but so is time in the market.

Lesson 4: Intuition To Realistically Double Your Money

Most people intuitively know that their money won’t double in value every day like the magical penny; however, the thought experiment opens the door to talking about realistic growth rates for investments are and providing rules of thumb for people to use.

The Rule if 72 helps you estimate how long it will take for your money to double. If you divide 72 by the rate of return you expect, it will tell you roughly how long it will take to double your money. For example, if you have $1000 and expect to earn 8% each year, in 9 years (72 divided by 8), you would have ~$2000.

I also point them to calculators and research on the real rate of return (i.e., adjusted for inflation) over historical periods. For example, between 1985 and 2014, McKinsey found that real total returns for stocks in the US and Western Europe average 7.9% each year; however, these were higher than the 100-year averages and, perhaps more alarmingly, much higher than what McKinsey thinks the future rate of return will be.

Lesson 5: If It’s Too Good To Be True, It Probably Isn’t True

While I devote a lot of time later in my workshops to financial advice and the importance of only working with fiduciaries, the magical penny is a helpful reminder that money won’t realistically double every day or every year. What I tell attendees is that if someone is trying to sell you a guaranteed investment that they promise will double your money in a year, you should be highly skeptical and run.

Or in other words, don’t give them even a single penny!